Today, there is only one thing on the menu: The Fed.

The Fed Cuts Rates 0.25%

In a move that surprised nobody, the Fed lowered the federal funds rate by 25 basis points, or 0.25% this week. For those interested, the federal funds rate is the interest rate banks charge each other for overnight loans. Now that that’s out of the way, here’s what you need to know:

- This is the first time since December the Fed has touched rates.

- While some analysts and politicians were calling for a larger cut, only one committee member voted for a 50-basis point reduction.

- In their economic projections released yesterday, the Fed indicated they expect two more 25-basis point rate cuts this year, and one in 2026.

- While their statement mentioned that “job gains have slowed” and “uncertainty about the economic outlook remains elevated,” they did raise their forecast for economic growth this year to 1.6%, from 1.4% in June. All of their other economic forecasts were the same as they were back in June.

- The financial markets were happy with the move until Fed Chair Powell referred to the cut as “risk management.” They were looking for a stronger commitment to lowering rates, but luckily, they seem to have gotten over their disappointment.

So how will this impact rates on credit cards and loans?

While credit cards and other short-term borrowing rates should come down a little bit, don’t get too excited. Remember that the Fed cut rates a full 1% last year, and there was very little change in short-term lending rates.

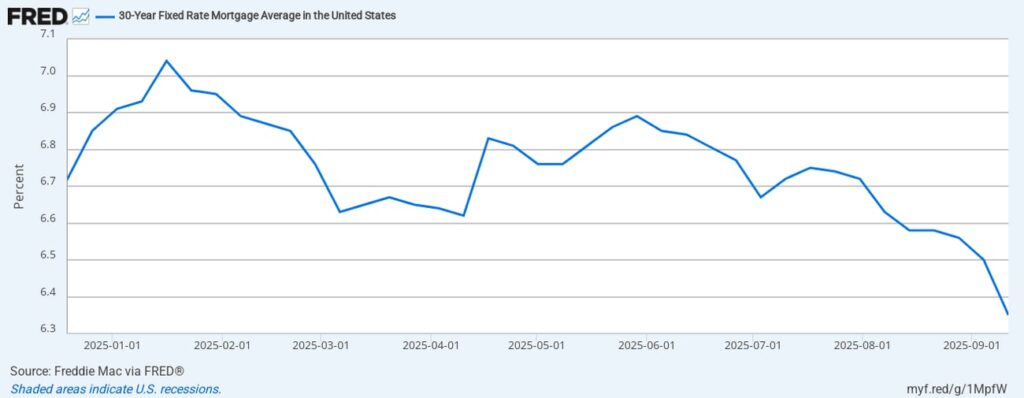

As I’ve said dozens of times before, there is no direct relationship between Fed rate actions and mortgage rates. After the Fed cut rates 1% last year starting in September, mortgage rates went up the next few months from 6.09% to 7.04%. It’s the rate on 10-year U.S. Treasurys that has the biggest influence on the mortgage market. Those rates are determined by the investors who buy those bonds, and many of them will continue to keep an eye on inflation, which remains higher than the Fed’s target.

{kind=link}

That said, I do expect mortgage rates—which just fell to an 11-month low—to continue falling in the short run, but not because of the Fed’s actions. Long-term rates go down when the economy weakens, as slower growth will reduce the risk of inflation. The weak hiring numbers over the past few months combined with proposed massive -911,000 revision to job growth in the year ending March 2025, clearly show a weakening economy.

That said, any higher-than-expected inflation report or sign of a sharp rebound in economic growth could raise inflation fears and bring mortgage rates right back up.

The bottom line is that mortgage rates fluctuate daily and are influenced by the economy, inflation, market volatility, government debt, and investor sentiment. While the Fed’s actions are important to the economy, they are not what drives mortgage rates. To help prove my point, let me leave you with a chart of the average 30-year mortgage rate since the Fed last touched rates on December 19, 2024:

You can see how often mortgage rates have gone up and down since then, even though the Fed made no changes to short-term rates during that time.

Leave a Reply